A UAE bank does not review corporate account documents as a paperwork exercise. It uses them to understand the legal entity, the people behind it, the business activity and the risk profile of the account.

This checklist supports the main guide on corporate bank account opening in the UAE. It focuses on documents only, so it does not repeat the full process.

What You Need to Know First

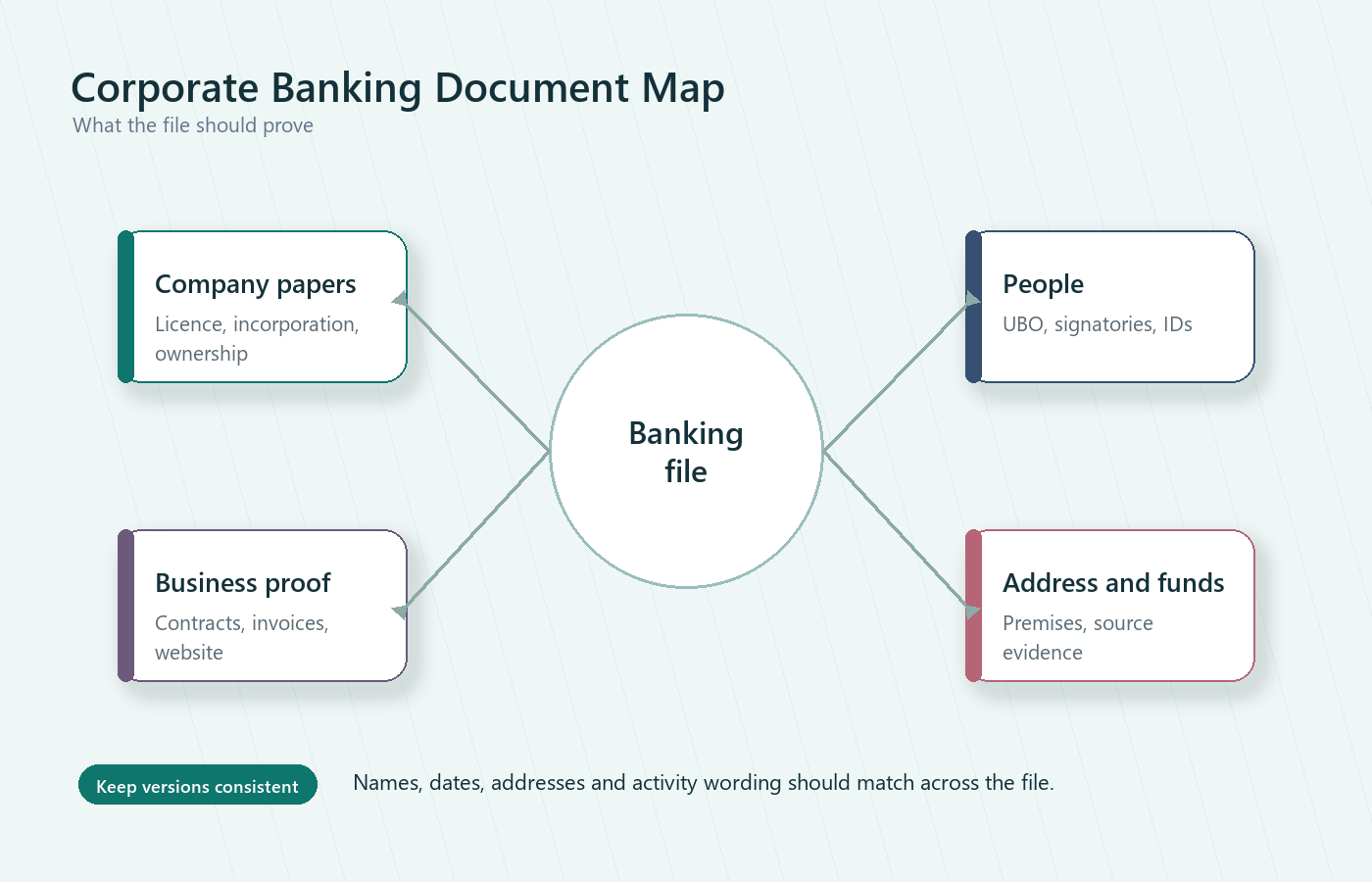

The documents required for corporate bank account opening in the UAE usually fall into five groups: company registration documents, shareholder and signatory identity documents, ownership and UBO information, proof of address, and evidence explaining the business model and source of funds. Banks may ask for more documents if the company is new, foreign-owned, multi-shareholder, trading internationally or operating in a higher-risk activity. The goal is not just to upload files. The goal is to give the bank a consistent KYC file that proves who owns the company, what it does and how money will move through the account.

Free download

UAE Business Bank Account Documents Checklist

Download the full documents checklist as a printable PDF and an editable Excel tracker, plus a bank-readiness worksheet.

Need help preparing bank account documents? Submit a request and compare up to 5 verified UAE consultants - free, no obligation.

Preparation aid from Emirae.Pro - not an official government form and not legal, tax or immigration advice. Last reviewed 3 July 2026.

The Core Document Groups

Most UAE corporate bank account files are built around these groups:

- Company registration and licence documents.

- Shareholder, director and authorised signatory identity documents.

- Ownership, control and UBO records.

- Address proof for the company and, often, key individuals.

- Business profile, source of funds and expected transaction evidence.

| Document group | Why the bank asks | Common examples |

|---|---|---|

| Company documents | To confirm legal existence and activity. | Trade licence, incorporation certificate, MOA or AOA. |

| Identity documents | To verify shareholders and signatories. | Passport, visa, Emirates ID where applicable. |

| Ownership documents | To identify control and UBOs. | Share register, UBO declaration, board resolution. |

| Business evidence | To understand activity and money movement. | Contracts, invoices, website, business profile. |

Company Registration Documents

The bank first needs to confirm that the company exists and is allowed to carry out the activity you describe. Prepare:

- Valid UAE trade licence.

- Certificate of incorporation or registration, where issued.

- Memorandum and Articles of Association or equivalent constitutional document.

- Share certificate or shareholder register for free zone entities.

- Board resolution authorising account opening and naming signatories, if required.

- Corporate structure chart if there are corporate shareholders.

Practical warning

If the trade licence says one activity but your business profile describes another, the bank may pause the file. The activity, website, invoices and explanation should all point in the same direction.

Shareholder and Signatory Documents

For individuals, banks commonly ask for passport copies, visa copies where applicable, Emirates ID for UAE residents, contact details and sometimes CV or professional background. For corporate shareholders, banks may request parent-company documents and ownership chains.

- List every shareholder and authorised signatory.

- Confirm whether each person is resident or non-resident.

- Prepare identity documents in a consistent format.

- Check expiry dates before submission.

- Prepare certified or notarised copies if the bank requests them.

The bank is not only verifying names. It is checking whether the people behind the company match the business risk it is being asked to onboard.

UBO and Ownership Information

UAE banks need to understand the ultimate beneficial owner structure. This is aligned with the wider UAE transparency framework, including real beneficiary procedures discussed by the UAE Ministry of Economy.

Prepare a clear ownership explanation if your structure includes:

- Multiple shareholders.

- Corporate shareholders.

- Holding companies.

- Nominee arrangements.

- Trusts or offshore entities.

Proof of Address

Proof of address is often treated casually, but it can affect KYC review. The bank may need to verify both the company’s UAE address and the residential address of signatories or shareholders.

Common address documents include tenancy contracts, Ejari, lease agreements, flexi-desk agreements, utility bills, bank statements or official correspondence. For a dedicated explanation, use the proof of address requirements for UAE corporate banking guide.

Source of Funds and Business Evidence

Source of funds is separate from the general document checklist because it often needs a narrative, not just a file. Banks may ask how initial capital was earned, where operating funds will come from and who the expected counterparties are.

Useful documents can include:

- Personal bank statements.

- Corporate bank statements from an existing business.

- Sale agreements or dividend evidence.

- Contracts, invoices or purchase orders.

- Supplier and customer lists.

- Business plan or profile for new companies.

See source of funds documents for UAE banking cases for the deeper compliance-focused guide.

How to Organise the File Before Submission

A strong document file is easy for the relationship manager and compliance team to read. Use clear filenames, group documents by category and prepare a short index.

- Create one folder for company documents.

- Create one folder for each shareholder or signatory.

- Create one folder for address proof.

- Create one folder for source of funds and business evidence.

- Add a one-page business profile summarising activity, owners, customers, suppliers and expected transactions.

Special Cases That Usually Need More Evidence

Some companies need more than the basic list because the bank has to understand extra risk or complexity. Prepare additional support if your company has:

- Corporate shareholders: parent company documents, ownership chain and authorised signatory evidence.

- Non-resident owners: overseas address proof, foreign bank statements and clearer identity verification.

- Trading activity: supplier details, purchase orders, invoices, shipping routes and expected countries.

- Consulting activity: service descriptions, client examples, founder CV and contract templates.

- New company with no revenue: business plan, founder background, proposals and source of initial capital.

These additions do not guarantee approval, but they reduce the number of unanswered questions in the first review.

If your file is already under review and questions keep repeating, read why UAE corporate bank account applications get delayed.

When Documentation Support Helps

Some founders can prepare a clean file themselves. Others benefit from support when the case involves non-resident owners, corporate shareholders, complex UBO structures, missing address evidence or prior rejection.

Emirae.Pro has dedicated pages for KYC documentation support and corporate bank account assistance if the file needs review before submission.

FAQ

Are the same documents required by every UAE bank?

No. Banks share common KYC themes, but each bank has its own forms, risk appetite and document requirements.

Do free zone companies need different documents?

They usually provide free zone incorporation documents instead of mainland documents, but banks still ask for ownership, identity, address and business evidence.

Is a business plan always required?

Not always, but it is useful for new companies, complex activities, consulting firms, trading companies and non-resident founders.

Do banks need original documents?

Some banks may ask to see originals or certified copies. Others may start with digital copies and request originals later.

What if I do not have invoices yet?

New companies can use contracts, proposals, supplier quotes, a business profile, website, founder background and expected transaction explanation.

Can missing documents cause rejection?

Yes. Missing or inconsistent documents can cause delays, repeated questions or rejection if the bank cannot complete KYC.

Need Help Choosing the Right Setup Path

If you are preparing a UAE company bank account application and want a second view on documents, bank fit, KYC risk or next steps, Emirae.Pro can help you compare the right support options without turning the article into a sales pitch.

You can compare UAE business consultants on Emirae.Pro, submit a request, or contact Emirae.Pro if your case involves setup, banking, tax, visas, compliance or documentation.

UAE Business Setup Specialist

Krystyna Sokolovska is a UAE business setup specialist who helps founders, independent professionals, and growing companies navigate business launch decisions in the Emirates with more clarity and less risk. Her work focuses on the practical side of entry into the UAE market — choosing the right setup path, understanding licensing options, preparing for banking, planning visa steps, and avoiding common mistakes that slow companies down.

Need help with this?

Submit a request and receive tailored offers from verified UAE business consultants. Free, no obligation.